PRIV and PRIV Accessories: June 30th Edition

RIP SSGA, gone but not forgotten.

Welcome to your weekly update on the SPDR® SSGA IG Public & Private Credit ETF (PRIV) and soon to be the SPDR® SSGA Short Duration IG Public & Private Credit ETF (TBD) too.

Thanks for reading!

This Week:

We’ll discuss the death of SSGA. I’m adding another private asset to our analysis and also tracking the par value changes for our private-ish and really private stuff.

Life Stuff:

I continue to have really fun and thought-provoking conversations with both clients and folks in the industry. My absolute favorite part of being an “outsider” aka consultant is that I can talk to anyone and can deep dive into topics. When a client come in with a novel/new to me idea or product I still get pretty jazzed up.

For those keeping track at home, I’m 6/9 days biking to my pool, swimming, biking back, and taking my dog for a light jog.

Ok, let’s dive and talk about PRIV.

N-A-V Moon

If you missed my Emergency Post go read it!

Here’s the NAV History file - Updates daily

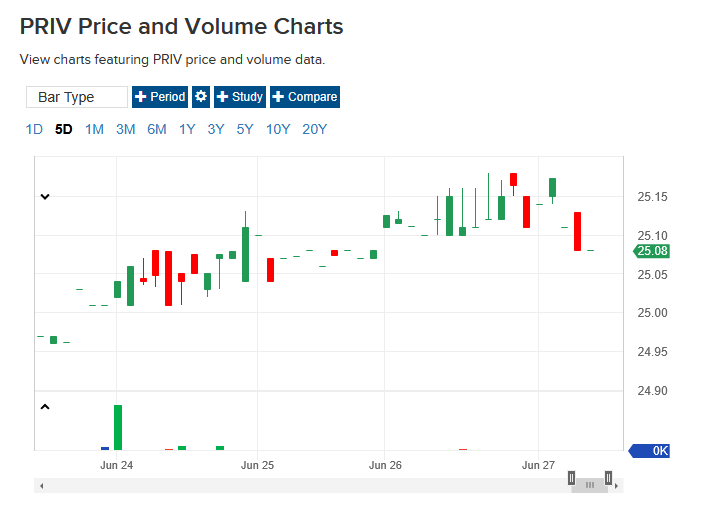

Shares, glorious shares. Last week saw the first share creation since launch week. 650,000 shares were created by APs and the net assets jumped up 16+mm to around 71 million. As discussed in the emergency post, I have my suspicions that this is still all being done for a single client/small RIA group.

Volumes:

One. Million. Dollars.

Also, last week I discussed a $374k trade that I couldn’t explain. I have been sent proof (thanks readers!) and it was a NAV trade that happened late.

Ok, so we had a ONE MILLION DOLLAR

day.

This volume happened on June 24th, it looks like the remaining existing shares got yanked off of someone’s books en route to the share creation event on June 25th.

My theory seems to be someone borne out by the activity the rest of the week. Besides this huge single day (really one trade) the volumes are back to their relatively doldrum like levels. We’ll see how that plays out moving forward.

Holdings:

I covered that there were no new adds or drops in my emergency post as of June 25th. There were no changes after that. We’re going to do a bit of existing holding analysis here.

I’ve covered the FIDES changes, here’s the rest of the private upsizing.

AGL Energy is now getting tracked along with the AP assets and has added 500k.

The rest of these assets are CLOs with private-ish stuff in them. Some bank loans, some MBS. The interesting thing is the general lack of price impact from these purchases. I don’t know whether that’s because they had good marks and didn’t pay too much of a premium or because they’re just using whatever assumptions. Full disclosure, I do NOT pay much attention to these holdings because they exist in plenty of other products and there is generally publicly available paperwork on them.

Issues, Marks, and Meta

Issues:

Nothing major this week. I’m glad to see that we’re getting a little more interesting movement. I think (knock on wood) that this quarterly rebalance might be a cadence moving forward. Who knows.

Marks:

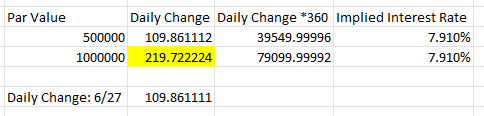

Here’s a fun chart!

So now I’m tracking AGL Energy, which I still have very little detail about beyond my previous findings. It’s something to do with coal in Australia. Who knows. There was a huge change in mark on 6/9. I have no idea what caused it. As well, when they bought another chunk, it looks like it was at a premium to their previous marks, similar to AP FIDES.

It seems like they may have forgotten to update their accrual metric to account for the larger size as they only marked the position up by the original assumed interest rate.

They’ll fix it now, hopefully.

This is SO cool looking but doesn’t show much. The upsizing in AP Fides skews it into the stratosphere.

Same goes here. I may need to just force an artificial maximum next week so we can get back to a decent visual but for this week we can enjoy the distortion. Some interesting price movement across these assets but ultimately I can’t give a good reason why any of the movements are happening.

Meta:

RIP SSGA. State Street Global Advisors is gone forever.

Hail the new king State Street Investment Management.

They have a really ugly new website design that looked vomited out by WIX (shout out to them for my terrible website design). Whichever consultant got paid a few hundred k for this. You’re evil and I hate you.

There is a LOT of commentary out right now about public access to private assets. Cliff Asness was on the Money Stuff podcast with friend of the stack Katie Greifeld and hopefully one day friend of the stack Matt Levine (we can dream!) and had some fun commentary (as he usually does).

Another friend of the stack Dave Nadig got quoted chatting on a panel with Joanna Gallegos from BondBloxx at the M* convention in Chicago last week.

I like the distinctions being drawn between the different levels of opacity within the asset class now. This is a line I’ve drawn for quite awhile now and why I don’t bother to cover most of the “private” assets. I consider them public-like instead of private.

These conversations are not happening in a vacuum. There are a number of folks that I’ve seen come around to saying “Maybe these truly opaque pieces can stay where they are”.

There are a number of truths that people need to acknowledge.

Intentionally illiquid products must pay investors a premium for that illiquidity.

That illiquidity is a feature for these investors. They are willing to lock up their money for xx years in return for making extra either over the course of the investment (private credit) or at exit (private equity).

This feature also allows them to avoid volatility and avoid having to mark their portfolios and report potential losses/defaults/refinancings.

Companies taking on private debt usually prefer to be answering to one group/sponsor. They know if there is an issue with payment or other corporate action, they can call up the GP and work something out privately and not destroy their reputation.

ETF’s basically wreck all of this.

The process of bringing these illiquid assets to retail investors in an ETF format requires two things.

Daily liquidity (read: volatility)

Accurate pricing

The first tends to beget the second and in doing so, negates the entire raison d’etre of private credit.

I just don’t see how these things meet.

If you liquitize private credit and remove the premium, you’re left with… (mostly high yield) public credit. I agree that public markets could be improved but this whole exercise just seems like a loop function.

Maybe I’m wrong but I haven’t had anyone win the argument yet.

Until next week, thanks for reading!

Other Stuff:

Go read these people:

Dave Nadig : Nadig.com

Tony Dong : Linkedin

Jeff Ptak : Substack | Morningstar

Tematica Signals : Substack

Phil Bak : Substack

CovenantLite : Substack

Brent Sullivan : Substack

Leyla Kunimoto : Substack

also anyone I subscribe to on Substack. I actually do read them!

Thanks for reading.

If you want to chat about PRIV/other topics or hire me, please reach out to cmacwilliams@outerbeachc.com, connect with me on LinkedIn, or shoot me a note on Signal at @ ConorMac. 76.

Disclosure: I own one share of PRIV, none of this is investment advice and is presented solely for educational purposes.